Non-Traded BDC Software Exposure & Industry Classification Analysis

- Mar 24

- 3 min read

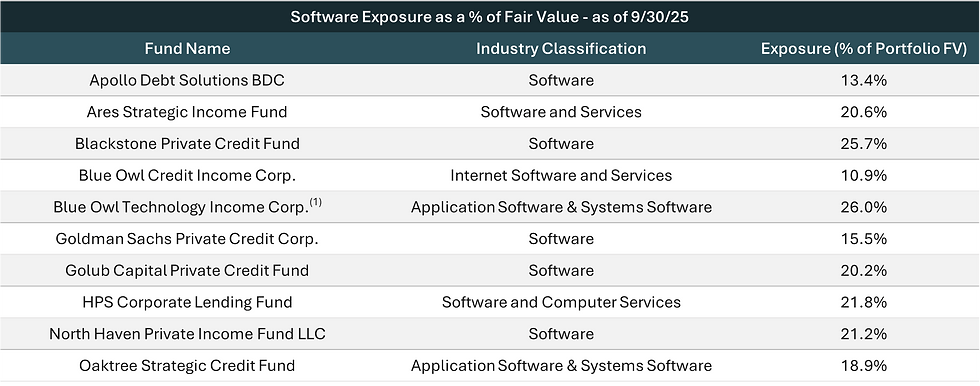

As AI continues to evolve and new capabilities emerge, investors have been trying to assess the potential impact on specific industries and companies. Recent developments in AI have amplified concerns that investments in software companies may be vulnerable to AI-related disruption, which has led to increased scrutiny regarding the software exposure of non-traded BDCs. By looking at the disclosed software exposure of some of the largest non-traded BDCs, we can see that software-related investments can comprise a significant portion of these funds’ portfolios.

However, challenges arise when attempting to compare the software exposure each fund may have. As seen in the table above, industry classification methodologies vary between funds, and what one fund considers a “software” investment, another may classify as something else entirely. Comparing how different funds classify the same portfolio companies make these differences more concrete. The following table compares how an investment in Kaseya Inc. was classified based on disclosure in each fund’s Schedule of Investments as of September 30, 2025:

While a uniform industry classification standard across funds may improve the accuracy of industry exposure comparisons, even when funds utilize the same industry classification standard, differences arise. Both Ares Strategic Income Fund and Blue Owl Technology Income Corp. disclose the use of the Global Industry Classification Standard (GICS®) in determining how investments are classified. However, when classifying RealPage, Inc., an investment held by both funds as of September 30, 2025, Ares Strategic Income Fund classified the company as Software and Services while Blue Owl Technology Income Corp. classified it as Real Estate Management & Development.

NOTE: Industry classification is based on each fund's disclosure in its Schedule of Investments as of September 30, 2025.

Additional variation may arise due to certain funds choosing to classify a portfolio company based on the products or services it offers, while others may classify portfolio companies based upon the end market the products or services are intended for. Portfolio companies may also have diversified operations, allowing them to fit into multiple industry classifications. Take Finastra USA, Inc., for example. The company describes itself as a fintech company that provides financial software solutions and systems. Classifying the company as operating in the Financial Services or Software industries may both be defensible, but the example highlights that funds have discretion when a portfolio company doesn’t fit cleanly into a single category.

The discretion funds exercise in classifying portfolio companies makes it difficult for investors to accurately assess software exposure and draw meaningful risk comparisons across funds. As the sample above illustrates, the disclosed software-related exposure may be overstated or understated relative to peers, making the reliability of these values questionable for comparison purposes. Accurately comparing software exposure between funds requires a deeper understanding of each fund’s classification methodology and the underlying investments driving that exposure, which places the burden on investors to understand potentially hundreds or thousands of holdings within and across portfolios.

Sources:

SEC Company Filings for:

MSCI, The Global Industry Classification Standard (GICS®)

Disclaimer: The information contained in this research note has been assembled using publicly available information. While SK Research and Due Diligence, LLC (“SKRADD”) believes it to be reliable, there is no guarantee that all of the information contained in this research note is or will be accurate. This research note does not constitute investment advice and is intended for informational purposes only. This research note does not constitute an offer to sell or the solicitation of an offer to purchase, nor should it be considered a recommendation of any security referenced herein. This publication is copyrighted, and no person is authorized to make use of the information presented herein without the express written permission of SKRADD. SKRADD is under common ownership and control with Snyder Kearney, LLC, a law firm that conducts due diligence reviews of alternative investment programs, including non-traded real estate investment trusts.